Let's talk money.

I grew up in a single parent household and was lucky enough to not only have a supermom but also a business savvy mom. In school we are taught all that we need to pass exams, but these lessons don’t include personal finance. Most people get into the real world and have no concept of money management or where to even begin.

I have a thirst for knowledge in this area and a passion for sharing what I know to encourage others to take money management and personal finance seriously. When it comes to money management, there’s nothing better than knowing your bills are paid, your savings is growing, and you have some extra funds to “do you.” If you haven’t gotten started just yet or would like to add on to what you are currently doing, here are some tips to jump-start the process:

1) Visualize what you are working with!

Have you ever heard people say that they are visual learners? Well, I consider myself one. Keeping an excel sheet is a bit old school but I love the flexibility in changing numbers, using formulas, and the ease of sitting at my laptop and being able to see all my funds at once. Depending on your pay schedule, list out which bills you plan to pay with what check. After you add these things up, subtract from your net pay and what's left over, you can play with! Now if you are more tech savvy and prefer to have your budget at your fingertips, consider looking into apps such as Mint, which allows you to have convenient access through your smartphone. Remember, the key to budgeting is to track your spending! By doing so, you’ll know where to cut back and where you have room to wiggle.

2) Don't forget to pay yourself.

Although we can get caught up in the hustle and bustle of life, there’s nothing like knowing you have some “tuck-away” funds. Before you do anything additional with your money, put away a set amount of funds into your savings account. Make saving a priority; don’t wait until you’ve spent most of your money and only save what’s left. “The goal of paying yourself first is to help make sure your future self’s key financial goals are covered, including building up an emergency fund, contributing to retirement and saving for any other long-term goals (Forbes).”

3) Have a savings account that is not tied to your primary bank account.

We all know the saying “robbing Peter to pay Paul.” This is exactly what happens when we co-mingle our funds, so to speak. You say to yourself you’re going to save $100 a check but once you start getting down to the last few dollars in your checking account, you start to slowly dip into your savings. How come? Because it's so easy. All you have to do is transfer the money and it’s immediately available. A solution for this would be to keep your "real" savings separate. I opened a savings account with a completely different bank and chose not to get a debit card for it. The best part of this account you ask? It takes three days to transfer money into your checking account. By the time you would receive the money, guess what? Those shoes or that bag isn’t so important.

There's also Digit. This free website and app studies your financial moves and automatically transfers money from your bank account to your Digit Account. They will send you daily, fun texts with updates of your balances and transfers. You can choose to save more, pause savings or withdrawal your money via text as well. Your money is FDIC insured and they have a no-overdraft guarantee.

4) Know Your Debt. Then, Knock It Off!

Make it your business to know what's out there in your name! Lots of people get duped for being uninformed. You can and most certainly will be penalized for not paying bills in your name, even if you knew nothing about them. Pull your credit report, everything you need to know will be included. Next, make a list of your debt from the smallest amount to the greatest and start knocking them off one by one. Each time you finish one, take the extra money and apply it toward the next debt. As you begin to see your debt decrease, you will feel motivated to keep going.

5) Did somebody say rainy day?

Now I'm sure we all know how it feels to get caught in the rain without an umbrella! The same applies to unforeseen circumstances that may leave you in a bind and needing some quick funds. Most financial advisors recommend having at least 3-6 months of living expenses saved. Yes, you heard me right, 3-6 months and that includes rent, monthly debt payments, and whatever other obligations you have to take care of. For some of us when we add that up, that number can scare us so I recommend starting small. According to financial author Dave Ramsey, an emergency fund of $1k is a good place to start. Set a plan, take your time and you'll get there. Once you reach that $1k goal, set small goals to get yourself to that 3-6 month cushion. “You cannot expect victory and plan for defeat” (Joel Osteen). Small victories are better than none!

6) It's never too early to start saving for retirement.

Unfortunately, by the time many of us retire, the social security program may be depleted. This is one less source of income a retiree will have to look forward to. Don’t let this discourage you, take advantage of the many options that are available to you. More often than not, we may approach situations with the “we have time” mind frame. Well honey, time flies and when it comes to investing, the earlier you contribute, the greater your return. Contact the HR rep for your employer and see what options are available to you (ex: 401(k) or pension). If your job doesn't provide you with options or you prefer to do your own thing, look into options such as a Roth or Traditional IRA. Doing your research is key; then go with the best option for your financial situation. There’s a huge misconception that you should wait until you make more money to save. This couldn’t be more inaccurate. As you get older, in most cases you have more responsibility (kids, spouse, mortgage, etc.) and these things will be just additional reasons for why you can’t save. Bottom line is it may never “feel” like the right time. Start saving now!

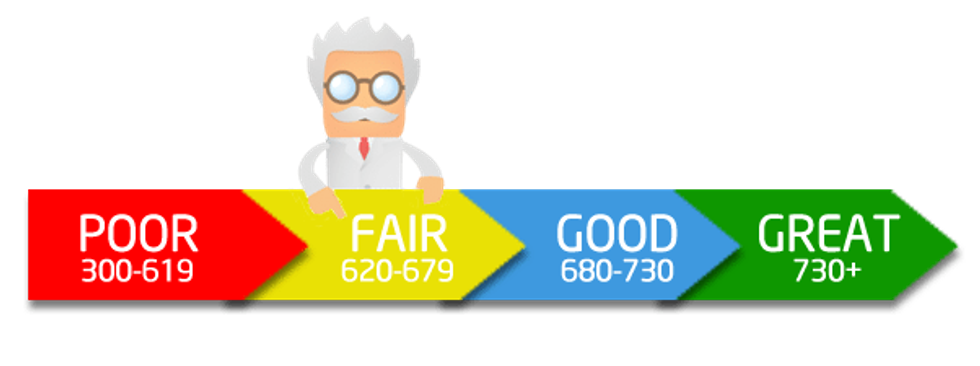

7) Your Credit Score…Know It!

The dreaded score that gets ruined before you realize its importance and why you need it. I got my first credit card in college. My mom warned me about how debt can easily add up but at that age I didn’t care. All I knew was that some bank was crazy enough to give me a credit card. Fast forward to now, I play no games when it comes to my credit and paying my bills on time. I’ve even gone as far as to not carry any credit cards in my wallet. Here and there I may carry one for emergencies but I hate to be tempted by that bag or those shoes! If you haven't already, pull your credit report on FreeCreditReport.com at least once a year. Go over it thoroughly, make a plan to pay outstanding balances, and dispute any charges that are erroneous or unwarranted. This report and your score speak to your credit worthiness; it could be the determining factor of whether you get that fabulous house or not.

8) Don’t be Pimped by Your Life!

Many times we get stuck being in situations we despise because we don’t see a way out. This goes for relationships, jobs, business ventures, etc. Having security, a cushion, or being stable could mean the difference between leaving that job you hate and following your dreams or staying at that 9-5 because you have no money saved up and need to make ends meet. Don’t get me wrong, there’s nothing wrong with a 9-5, that’s what I do now. Let’s keep it real, many of you desire more or if given the opportunity would be doing something else. The only constant in life is change, so be prepared. Now when that unplanned event happens or you just wake up one day and want to jump ship; you will be ready! A lot of what I included in this article is just a snippet of how good money management can lead to financial freedom. As a result, financial freedom can lead to a greater quality lifestyle.

[Tweet "There's beauty in stacking your coin and being able to direct your own life!"]

Have your finances ever been in shambles? What are some steps that you took to get back on the right track?

Germeen is a NYC auditor pressing her way through the jungle gym known as corporate America. Her thirst for adventure has been proven by the stamps on her passport and her hunger for new experiences is demonstrated in her commitment to live life to the fullest. She is a self-proclaimed control freak and personal finance enthusiast somewhere overdosing on life.